As mentioned in my post on the Union Budget FY 2013, I

would like to share these 2 Open Letters, addressed to Mr. Finance Minister, in

response to the Budget. The reason I picked these two is that they offer very

different vantage points; one is from the perspective of a student, and the

other is from the perspective of a tech-entrepreneur. Both letters provide good insight on the kind

of impact the Budget's proposals would have on everyone, and how this Budget, just like all its predecessors, is not a proactive one.

1. Why I didn’t like the budget: A

student’s view of Budget 2012

Dear Finance Minister,

I hated hearing that long budget speech

of yours. Who wants to know if there was an increase in the paddy yield? All I

cared about was going to the US, getting a foreign degree and making some

money. But do you care?

You are now giving my parents second

thoughts about sending me abroad. So what if there’s no service tax on

pre-school and high school education? That’s in India. Of course I am not

bothered!

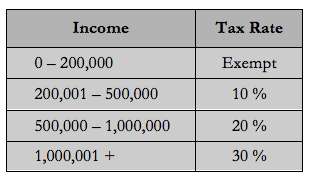

You increased the service taxes on all

other things from 10 percent to 12 percent. This obviously means my father has

to pay more for my GRE tuition and TOEFL tuitions.

For all you know, he might just decide

to keep his money in his savings account for it to grow; as you announced that

will give him higher income tax exemptions on it and maybe he’ll send me to a

college in India. That’s not what I want.

He’s already talking about reducing my

pocket money and now you have given him good reason to do that.

The education loan I would take to

study abroad won’t come cheap. On top of that, eight years is all I have to repay

back the loan. Eight, just eight? Couldn’t you, our finance minister, increase

it to 10 years, at least?

Yes, I know you are allocating funds to

research centres in India, but I still want to go abroad to study.

You promised to ensure better flow of

credit to us, by proposing a Credit Guarantee Fund. But when will that be set

up? I want to go abroad the next year as soon as my I am done with high school,

but this ‘credit thing’, I am sure, will not be set up so soon. The way India

functions it will take another five years. Can you promise you will set it up

this year?

You also proposed to set up more

schools in rural areas. Ok, I understand development. But what about women’s

development? Girl child education and all that? Nothing.

No easy loans even for the girls, while

the interest rates will continue to remain at par with the boys.

And even if I forget education abroad

for a moment, what about that bike that my father was supposed to give me next

month? You’ve made that expensive too. And now that will have to wait too.

Sincerely patient,

A student who did not like your budget

2. Mr. FM, why don't you ever think of

entrepreneurs?

Dear FM,

I looked you up on Facebook but

found a cold 'page'. I checked on Twitter, but came across some fake ids. I

searched on Linkedin but you don't seem to be there. I gathered that I can't

hang out with you on these internet-mobile places I hang out in, because you

probably don't visit them!

Let me come to the point. I read your

budget speech with interest (all 14,234 words of it). Amidst your Pacific Ocean

of words, I found:

The word 'Startup' mentioned 0 times.

The word 'Internet' mentioned 0 times.

The word 'Mobile' mentioned 2 times.

The word 'Entrepreneur' mentioned 3

times.

Now, the word 'Farm' is mentioned 16

times and the word 'Agriculture' is mentioned 18 times. Sir, let me share with

you some interesting trivia. In another country, a couple of years ago, an entrepreneur created

a new agricultural community that invited farmers from all over the world.

The address of the farm was the

Internet. The place was 'Farmville'. Believe it or not, this Farmville 'thingy'

generated `300 crore of revenue in the first year. About 5 crore farmer

'players' signed up! When the Haiti earthquake struck, this community actually

garnered money and sent it to Haiti. To cap it all, the company, Zynga (that

started this virtual agricultural business), is actually listed on the stock

exchanges and is currently worth Rs 5,000+ crore!

Sir, just pause and think if Zynga was

created in India. You, sir, would have earned juicy service taxes, revenues

from corporate taxes, even would have a nice new age listed company on our

otherwise boring bourse. The point I am making, is that new age businesses of

the internet and new age entrepreneurs like myself, deserve a bit more

attention from you. Because we attract venture capital, we employ people,

we generate revenue, we pay our taxes and sometimes, even sell our companies

and bring the money home!

Sir, I don't like wearing suits and

ties; or coming to meet you in Delhi. But I can request you to help us in a few

critical issues, on behalf of the Internet, entrepreneurial community.

Consider These Two Examples:

A month ago, a team of four young

entrepreneurs came to meet me. In a couple of minutes, I figured two things

about them:

i) They came from families that a

decade ago, would have never dreamt that their children would be graduates,

speak fluent English and earn more money than their fathers ever did, all at a

young age.

ii) This quartet was smart. I mean

really smart. Smarter than anyone I had ever met!

This was a goosebumpy moment for me. It

signalled that the 'Indian Dream' was working. Despite all our odds, we were

producing local 'chaap' Einsteins! These four friends told me that they were

quitting their jobs and becoming Internet entrepreneurs. And they presented an

idea to me that blew my mind. They wanted me to mentor them, and I readily

accepted. I felt it was a 'Googlesque' moment (what may have transpired when

Google started up).

A week later, I got an SOS from one of

them. They wanted to acquire a web domain (a site name) that was available on a

foreign auction site since it was critical to their business. They requested I

help them. I readily agreed. What transpired is something I want to bring to

your attention.

To buy the domain, I needed to transfer

about $1,000 to a German company. They accept only 'PayPal' payments, but PayPal is

not available in India. When I wrote to the Germans they were flabbergasted!

They said, "PayPal 'is' the global payment platform for small

transactions".

But I had to tell them the Indian

government had severe restrictions in letting them operate here. I begged them

to allow me to wire the money to them. They agreed. When I started the

transfer, I realised that it was 'impossible' for a startup to manage the process

using the Indian banking processes! I had to sign some 8 forms, get my CFO and

his team to 'solve some major paperwork crosswords' and also pay for

certification charges.

Finally, I did get the domain, but

trust me, on their own, this hot start up would never have made it. The

over-regulated and complicated banking laws of India would have killed this

'google' in-the-making even before they started up.

After many years, I was able to woo a

senior gaming expert in the US to join me. All he wanted was independence and

esops. I gave him independence on day one, but the procedures to carve out

esops for a foreign national to be employed by an Indian company became a

mystery that would make even Dan Brown's Da Vinci Code look like an amateur

essay! It took a good four months to solve the riddle, and I went through hell

to keep Mr Gaming Rockstar motivated. He liked me and hung on, but now he is

really nervous about India and its laws.

Sir, the number of do's, don'ts,

regulations, forms, certifications, validations, permissions, etc that small,

startup internet companies require to comply with, kill our energy, excitement

and enthusiasm to grow. We need special treatment.

Let me say, that we are like delicate

flowers. We need special farming rules to grow. Give us those, and I promise

you, when we bloom, your treasury will be full. Not just with revenues but also

the scent of a new and fresh Indian Industry!

(The writer is a digital entrepreneur)